HDFC Ergo Optima Restore

Optima Restore Individual is the most suitable form of health plan that gives you restoration benefit when your sum insured get consumed fully or partly. Optima Restore not only gives you financial protection from minor to major illness but also provide you with health rewards for maintaining sound health throughout the policy tenure. With features like stay active benefit and multiplier benefit, makes Optima Restore health plan distinguishable from all the other health insurances.

| Sum Insured | Rs 3/ 5/ 10/ 15/ 20/ 25/ 50 lakhs |

| Age limit | 18 to 65 years for adults and 91 days to 25 years for dependent children |

| Lifelong Renewability | Lifetime |

| Tenure of the Policy | One/ Two years |

| Pre Policy Check-up | Required for 46 years and above/ taking 15 lakh or more as the sum insured |

| Sub-limits | No sub-limits on room and location for taking treatment at any network hospitals |

| Tax Benefits | Tax deduction while filing income tax on the annual salary under section 80 D of Income Tax Act due to the premium paid |

| Claim Settlement | 98% claim settlement ratio with regard to proper representation of documents. |

| Free Look Period | 15 days given to review the policy’s terms and conditions |

| Portability | Available (transfer all your previous policy’s accrued benefits to new optima restore individual) |

| Coverage Provided | Amount of Sum Insured | ||||

| 3 lakhs | 5 lakhs | 10 lakhs | 15 lakhs | 20/25/50 lakhs | |

| In-Patient Treatment | Covered up to the amount of sum insured | ||||

| Pre-Hospitalization | Up to 60 days | ||||

| Post-Hospitalization | Up to 180 days | ||||

| Domiciliary Hospitalisation | Covered up to the amount of sum insured | ||||

| Day Care Procedure | 140+ daycare treatments | ||||

| Cashless treatment | Available at network hospitals | ||||

| Ambulance Cover | Provided up to Rs 2000 per Hospitalisation for all types of sum insured | ||||

| Room Rent | No Sub Limit | ||||

| E-opinion on the investigation of critical illness | Can avail One time in a policy period | ||||

| Air Ambulance | Not Covered | Not Covered | Minimum of 2.5 lakhs per Hospitalisation and the maximum should not exceed the amount of sum insured in a policy year. | ||

| Daily Cash limit on selecting shared rooms | Rs 800 per day and maximum up to Rs 4,800 | Rs 1000 per day and maximum up to Rs 6,000 | |||

| Pre-existing diseases | Covered after a waiting period of 36 months | ||||

| Restoration of sum insured | 100% reload of sum insured on complete or partial consumption due to claims. | ||||

| Health check-up | Not Covered | Up to Rs 1500 once in every 2 years of the policy | Up to Rs 2000 once in every year of the policy | Up to Rs 4000 once in every year of the policy | Up to Rs 5000 once in every year of the policy |

| Multiplier Benefit | A minimum bonus addition of 50% to the sum insured on one claim free year and a maximum of 100%. The bonus received may subject to a reduction of 50%, if any claim is made in the succeeding year. While the basic sum insured will remain untouched. | ||||

| Critical Advantage Rider | Not provided | Provided | |||

Critical Advantage Rider

By choosing this additional cover, the insured can enjoy never-ending benefits attached. This cover gives you a treatment facility at network hospital present globally. In addition, it also gives coverage transportation expenses of insured and the attending member, accommodation expenses, post-hospitalization, and second opinion expenses. The illnesses covered under this rider are-

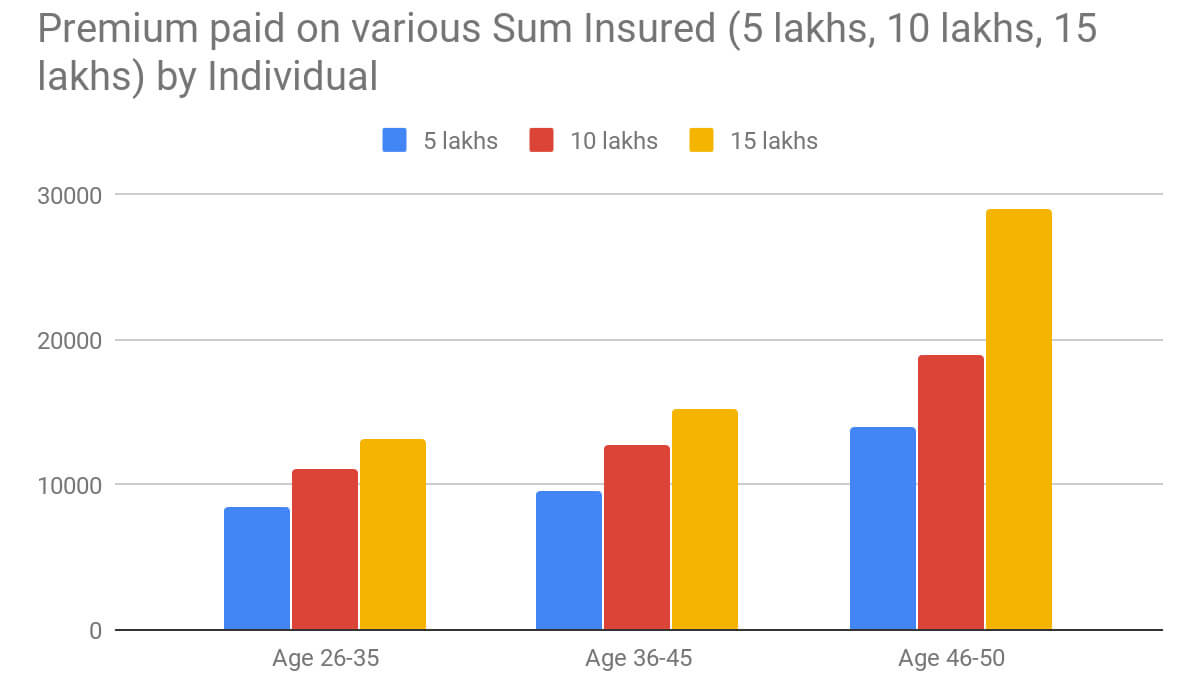

Here is the presentation of premium paid annually based on the age and sum insured value of the policyholder. The premium may change with regard to any medical conditions like pre-existing illness, smoking or drinking habits, and other illnesses. In the graph given below, it is assumed that the individual has no smoking habits and no pre-existing disease.

HDFC Ergo Health was formed with joint cooperation between two health leaders HDFC Ltd. and Munich Health. They conglomerated to bestow unprecedented health insurance services to individuals and their family.

HDFC ERGO Health Insurance (formerly known as Apollo Munich Health Insurance) keeps on launching new plans into the health insurance market like Optima Restore, Optima Vital, Easy health, Health Wallet etc.

The company also deals in travel insurance and individual personal Accident.

1. Does Appollo Munich pay for the claim made in the starting 30 days of the policy?

If any claim made during the starting 30 days, the company will not cover the expenses. But in case of accidental injuries to the body, the insurance provider will cover the expenses incurred.

2. What is the grace period in the policy?

The grace period is regarded as a period of 30 days where the policyholder is allotted a time limit to renew the existing policy. The grace period is used when the renewal date get elapsed due to negligence in the payment of premium by the policyholder.

3. Can we port our previous policy with Appolo Munich Optima Restore?

Yes, a policyholder can port or transfer all the benefits of previous policy to newly bought health plan after due allowances for waiting periods. Moreover, if you want to utilize portability benefit you have to inform the insurer 45 days prior to the renewal date of the policy.

4. Do we get reimbursement for the pre-policy check-up?

The company promises to pay or reimburse 100% of the expenses raised on medical check-up before buying the policy by the insured. The report of health check-up will be valid for 90 days maximum within which the policyholder submit the proposal of claim to get reimbursement.

5. What are the renewal discounts under Stay Active Benefit?

The discounts offered to insured on staying fit and healthy will be examined from the number of steps walked in a day. The count of steps will be tracked and calculated by a mobile application which should get downloaded from the inception of the policy within a period of 30 days. Look at the table to get precise information -

| Number of Steps on an average | Renewal Discount |

| 5000 or below | 0% |

| 5001 to 8000 | 2% |

| 8001 to 10000 | 5% |

| Above 10000 | 8% |

6. What is the notification period to make a claim?

The insured has to inform the insurance provider at least 48 hours before in case of planned hospitalization which claims may become important. In case of emergency hospitalization or any other medical issue, the insurer has to be notified within 24 hours after the happening of an event. No delay will be entertained by the company.

7. What is the procedure to avail a cashless claim?

8. What is the procedure for the reimbursement of claim?

9. What is the list of documents for settlement of claim?

For cashless settlement, the process is simple -

Last updated on 23-10-2020