Unlike health insurance, where you get protection against various ailments and medical procedures, Life Insurance provides a financial pool of savings after your unfortunate demise to your family. Life insurance comes in multiple forms and serves various purposes as compared to health insurance. Life insurance is one of the best ways to create wealth and secure the future of your family financially. When it comes to Life Insurance, choosing the best insurance policy can be exhaustive. Through this article we have discussed all the necessary factors that will help you in choosing the best life insurance policy in India. We have gathered all the necessary life insurance policy details so that you can find all the information at one place.

Recommended Videos

5 Big Benefits of Life Insurance

Best Life Insurance Policy in India

What is Life Insurance?

A life insurance policy includes a contract between a policyholder i.e. the customer and the insurer i.e. the insurance company that states that the policyholder will be given a lump sum amount after his unfortunate demise or a set period of time. The policyholder chooses a nominee on his behalf at the time of the commencement of the policy and the funds are provided to this nominee. Not all life insurance policies mature at the time of death. Many life insurance policies are bought for a certain period of time and mature after the decided tenure. There are a number of life insurance policies in the Indian market. They are as follows:

Term Life Insurance: As stated, term insurance is the purest simplest form of life insurance. The policyholder decides the tenure of the policy and pays the premiums to the insurer. Upon the demise of the policyholder the sum assured is given to the nominee. There are many forms of term insurance policies available.

Whole Life Insurance : These Plans remain in force till the policyholder is alive, provided required premiums are paid. On the policyholder's death, the plan pays a sum assured and a bonus (if any) to the nominee. In simple words, If a policyholder is alive till the policy tenure, the policyholder receives matured endowment coverage as a maturity reward under whole life insurance in India. A Whole Life Term Insurance can help you to leave a legacy for your children.

Child plans: A child plan in life insurance policy is dedicated towards building a financial corpus for your children. By estimating the time and the magnitude of financial needs of your children you can buy the best life insurance policy that can help your children at the crucial stages of their lives.

Investment plans:Investment plans come into the picture if you are looking forward to building capital for yourself. With investment plans, a part of your premium is investment in various financial tools and the returns are acknowledged by you. Investment plans come with a certain risk and therefore should be bought with great understanding. The frequency of investment can vary- weekly, monthly, and quarterly. Along with savings, you get the benefit of insurance coverage.

Pension plans: As suggested by the name, pension plans are meant for your post retirement days. You can choose the tenure of the policy and after the policy matures, it pays out in a lump sum or on a monthly, quarterly basis also pre-decided by you. Pension plans also come with tax savings. The benefits are given annually or once after reaching 60 years (depending on the insurer/policyholder). The plan offers a vesting benefit (maturity benefit) if the policyholder outlives the policy term.

Endowment Plans: Also known as traditional life insurance plans, the Endowment policy is a combination of a life coverage plan and savings plan. Along with life coverage, a policyholder can also save their funds regularly for a specific period. In case the policyholder outlives the policy term, the insurance provider offers a maturity benefit to him/her.Such policies can be used to build a risk-free savings corpus, and on the other hand, will provide financial protection to your family in case of an unfortunate event.

Unit-Linked Insurance Plans (ULIPs):Unit-Linked Insurance Plans offer a combination of investment and insurance. Under the same, a small portion of your money is used for life coverage, whereas, the rest of the money is invested in the market.

Money-Back Plan: In a money-back plan, the policyholder is eligible to get a specified percentage of their sum assured at regular intervals. This type of life insurance is ideal for those who want to invest with the benefit of liquidity.

Methods of Calculating Life Insurance

Most insurance companies say a reasonable amount for life insurance is six to ten times the amount of annual salary.

Another way to calculate the amount of life insurance needed is to multiply your annual salary by the number of years left until retirement.

Another method called the standard of living method is applied wherein you take the amount that survivors would need to maintain their lifestyle and multiply it by 20.

DIME (debt, income, mortgage, education). This is meant for a minimal amount of coverage that will cover family expenses in the event of an untimely death.

Key Features of Life Insurance Policy

A life insurance policy is much more than a source of coverage and thus consists of numerous features.

Death Benefits- Under a life insurance policy a sum assured known as death benefit shall be provided to the nominee in case of an untimely death of the life assured during the policy tenure which will help your financial dependents to fulfill their daily requirements and life goals.

Investment opportunity- Life insurance can act as an investment opportunity if one chooses to invest in ULIPs, Money Back and Endowment plans as these plans provide dual benefits of life cover and investments, such plans provide returns on investments.

Tax exemptions- Under Section 80C and 10(10D) of the Income Tax Act, 1961 one can avail of income tax benefits by investing in a life insurance policy.

Maturity Benefits- Various life insurance policies provide maturity benefits at the end of a policy term in case the life assured has survived the entire policy tenure.

Collateral for loan-Some life insurance policies offer loans against the policy feature which can help an individual to fulfill urgent financial requirements such as treatment for medical emergencies or help an individual to fulfill financial obligations.

What Are The Benefits of Life Insurance?

There are a plethora of benefits when you invest in a life insurance policy. Life insurance is a financial tool that facilitates an individual to create a safety net for their loved ones in case anything unforeseen happens to their life.

Financial Security: Along with life coverage, a life insurance plan also offers financial security to your loved ones in case of any uncertainty such as death or disability.

Secure Your Child's Future: A Life Insurance coverage will help to finance the educational and various other needs of your child such as their higher education, their marriage etc.

Retirement Planning: Life Insurance proves to be useful when you plan for retirement and acts as a financial cushion aiding financial independence post-retirement.

Comprehensive Plans: Along with financial support, it also serves as a long term investment option. Many conventional life insurance plans (such as traditional endowment plans) offer specific maturity benefits via multiple product options like maturity values, cash values, money-back, etc.

Insurance With Savings: Life Insurance plans allow the policyholder to get into the habit of financial savings. Saving cash over a lengthy time frame enables building a very good corpus to meet your economic necessities at every stage of life.

Tax Advantages: Life insurance policies offer you the benefit of the tax deduction on payment of premiums and provide a tax-free sum assured under Section 80C and 10(10D) of the Income Tax Act, 1961.

Loan Facility: Life insurance policies allow the policyholder to avail loan against their life insurance plan to meet any unforeseen situation.

How to Choose the Best Life Insurance Policy?

With the availability of several Life Insurance Plans in the market, it's quite confusing to choose the best among them. Considering one factor and ignoring the other can cause several issues at the time of need. Therefore, it is very important to go through each & every aspect before investing in life cover insurance.

We at PolicyX.com have mentioned a few pointers that will help you to choose the Best Life Insurance Policy:

Keep a close eye on the claim ratio: Before selecting a provider, you should check its claim ratio. This will give you a vague idea of the number of claims received & settled by a company in a single year. The company which has the highest ratio is your safe bet.

Background check: Due to the competition, a lot of companies have entered the market. Because of this, the industry is lacking quality providers. To be smart, you should check the background of each company. Whatsoever facts match your expectations should be the one for you.

Evaluation of sum assured: It is highly recommended to calculate your expected assured amount. Along with this, you can get an insight into premium calculation, which is done by the companies. Calculate your Life Insurance Premiums. Combine both the factors to know which company deserves your hard-earned money.

Customer reviews are important: Sometimes, the company may look brilliant from the outside but runs with bad intentions from the inside. The best way to find such companies is via customer reviews. These reviews are posted by those people who have experienced (first hand) how such companies function & whether or not they keep true to their promises.

24x7 Customer Service: PolicyX is always with their customers as we offer 24x7 customer care service.

Life Insurance Companies

Compare and buy the most suitable Life Insurance Plan from the below-mentioned IRDAI-approved Life Insurance companies.

Deciding the best life insurance policy in India includes various important factors such as past performance, claim settlement ratio of the company, its solvency ratio, customer support etc. Using all of the listed parameters and the annual report 2020-2021 published by the insurance regulator of India we have scrutinized the best life insurance policies for you.

A pure life cover that comes out with two death benefit payout options such as Level Sum Assured or Increasing Sum Assured.

HDFC Life Sanchay Plus

With several other benefits, the plan offers guaranteed returns to the insured and their family.

SBI Shubh Nivesh plan

A traditional savings plan that comes out with two investment option - Endowment plan & Whole Life Plan.

ICICI iProtect Smart

Offers 360-degree protection to your family, allowing in case of your unfortunate demise.

Max Life Online Term Plan Plus

An online term insurance plan that looks after your family's needs and offers 3 payout options for the family - lump sum one time, lump-sum along with a monthly income, or lump sum with increasing monthly income.

Life Insurance Riders

Riders are the add-ons that provide additional financial coverage to the policyholder. Some plans come with the in-built additional cover, however, generally, the riders need to be purchased separately by paying an additional premium.

Having additional coverage enhances protection for you and your family in case of death, disease, or disability.

Popular life insurance riders are:

1 Critical Illness Rider

Critical Illness Rider benefits the policyholders in case they get diagnosed with any of the critical illnesses listed in the policy document. The rider pays out the critical illness sum assured and allows the policyholders to concentrate on their treatments without worrying about the finances.

2 Accidental Death Benefit Rider

With the help of Accidental Death Benefit Rider, if the policyholder dies in an accident during the policy term, then a percentage of this additional sum along with the sum assured will be paid to the beneficiary by the insurance company.

3 Accidental and Total Permanent Disability Rider

This rider comes in force if the policyholder meets with an accident and is declared partially or permanently disabled. The rider pays the predetermined percentage amount and can be relied upon as the income source.

4 Accelerated Death Benefit Rider

If the policyholder is diagnosed with any life-threatening terminal illness such as leukaemia, cancer, AIDs, etc., this rider will pay a part of the death benefit and can be used for the treatment of the policyholder.

5 Waiver of Premium

Under this rider, if the policyholder is unable to pay his premiums due to the loss of income because of any unfortunate accident or injury, or disability, then all the future premiums will be waived off, and the policy will continue with no restrictions.

6 Term Rider

Term rider pays a fixed or monthly income to the beneficiary in case of the policyholder's demise. This rider offers extra coverage for death in addition to the base sum assured that is predetermined by the insurance company.

7 Surgical Rider

Surgical Rider assists the insured by providing financial coverage in case the policyholder undergoes an unavoidable surgery in India.

Factors That Affect Life Insurance Premium

A life insurance premium is an amount that is paid by the policyholders for a specified period and lets them enjoy the life insurance benefits. One can select their premium payment mode as per their needs.

Below are the few important factors that are considered by life insurance companies and can affect the life insurance premiums:

Age: Age is a significant factor while calculating the life insurance premium. As per the insurer's perspective, a young individual is less likely to suffer from age-related disease and pass away prematurely, and also has a higher chance of continuing their insurance policy for years. This makes younger individuals eligible for low premiums.

Lifestyle: If a person smokes/drinks/leads a stressful lifestyle, (s)he needs to pay higher premiums. This happens because such habits lead to life-threatening illnesses, lowering your life expectancy.

Gender: According to some surveys done in India, it is proven that women tend to live longer than men. Due to this disparity, women generally pay fewer premiums than men.

Medical History: If a person has a medical history of critical illnesses or is prone to health issues, then in such cases the insurance companies charge a higher premium.

Policy Tenure: The longer your policy tenure, the higher is the risk to insurance companies. Therefore, life insurance plans with shorter-term have lower premiums than long-term life insurance policies.

Why Should You Compare and Buy Life Insurance With PolicyX.com?

IRDAI Certified.

Gives online discounts.

Provides transparency.

Offers a simplified buying process.

IRDAI CertifiedGet Online DiscountsOverall TransparencyOffers Simplified Buying Process

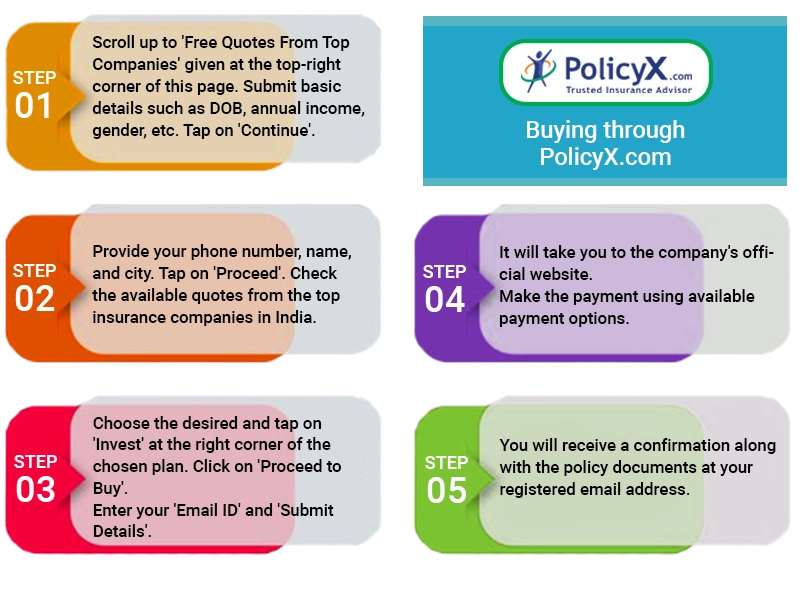

How to buy Life Insurance from PolicyX.com

PolicyX.com offers you a reliable platform where you can compare life insurance premiums and then choose the best one as per your preference. Check out the below steps and buy your life insurance now:

Go to the top-right corner of this page to find 'Get Life Insurance Quotes Online'.

Provide the required details and tap on 'Continue'.

Fill out your number and city to proceed ahead.

The page will show you all the plans that suit your preference.

Compare and select the best-suited plan out of available options.

Once selected, make the payment online and you will get the details of your policy on your registered email id.

What Are The Documents Required To Buy Life Insurance?

If you have decided to buy life insurance, there are a few documents that you need to provide:

Age Proof

Driving License, 10th or 12th mark sheet, Birth Certificate, Passport, Voter ID, etc.

PAN Card, Passport, Driving License, Voter ID, or Aadhar Card.

Income Proof

Latest form 16, salary slips of last 3-6 months, ITR (2-3 years), etc.

**Some plans require a medical check-up to make sure that the insured does not suffer from any chronic illness. The company may ask for other documents as well.

How To File A Life Insurance Claim?

If a claimant follows all the required steps, then filing a claim and getting a sum assured can become a very convenient and hassle-free task. Read ahead to find how a claimant can file a claim in India under the following scenarios:

In case of the insured's death, the nominee of the deceased will be able to claim in the following way:

Intimate the insurer about the death as soon as possible with all the important details such as time, place, and cause of death.

Submit needful documents and proof to the insurance company. This will consist of the insured's death certificate along with the claim form provided by the insurance company.

If the policy was assigned, the assignee will have to provide the documents. If someone else (apart from the nominee or assignee) is filing a claim, (s)he has to submit the legal proof of his/her relation with the insured.

If required, post-mortem, hospital, and attending doctor's reports have to be submitted.

In cases involving police inquiries, an investigation/survey report will have to be submitted.

Once the investigation is over, the insurance company will approve/disapprove the claim. The details of the same will be shared with the claimant.

In Case The Policy Is Matured

If the insured outlives the policy term, then he/she is eligible to avail all the maturity and surviving benefits, provided all the premiums have been duly paid. The procedure for filing a claim is as follows:

When the maturity date of the policy is near, the insurance provider will send an intimation to the policyholder with a discharge voucher (at least 2-3 months prior to the date of maturity).

The policyholder has to sign the voucher and send it back to the provider with the original policy bond.

If the policy is assigned to someone else (individual/entity), the amount will only be paid to the assignee who will give the discharge.

Conclusion

Life insurance is a must-have financial tool that can help you ensure the financial security of your loved ones while providing you life cover. A life insurance policy provides financial assistance to the life assured and their family members in difficulty. Keeping the current scenario in mind, a life insurance policy is essential for individuals who have financial dependents, if anything were to happen to an individual amidst the COVID-19 outbreak a life insurance policy can be very handy under such circumstances.

Life Insurance News

10 Apr

TATA AIA Life Insurance emphasizes financial planning through a new campaign

TATA AIA Life Insurance has launched a new campaign, ‘Karlo Shadi Ki Poori Taiyaari’. The campaign highlights that marriage is a new chapter of one’s life and it also means that we need to future-proof ourselves financially before embarking on this new journey with our partners. The CMO of the company said that with their term insurance products, guaranteed income products, wealth creation plans, and retirement plans the customers can effectively plan their futures and remain worry-free for life.

10 Apr

The IRDAI directs non-life and life insurance policies to be issued digitally

The insurance regulator of India, for the policyholder’s interest, has directed all the non-life, term insurance, and life insurance policies to be digitalized and held in an electronic form on their electronic insurance accounts (eIA). These e-insurance accounts will be offered by insurance repositories selected by the regulator. The IRDAI has granted the Certificate of Registration to four entities to act as ‘Insurance Repositories’ to open eIAs. Through these eIAs, the policyholder will be able to access and keep track of his/her non-life and life insurance policies online in one place.

10 Apr

Kotak Life Insurance joins hands with Jana Small Finance Bank

Kotak Life Insurance Company has partnered with Jana Small Finance Bank to offer life insurance products to its customers. This will offer benefits to 52 lakh customers of Jana Small Finance Bank. Kotak Life will provide tailor-made life insurance products to customers through their 781 banks spread across the nation in 22 states and 2 UTs.

28 Mar

IRDAI introduces new norms for surrender value of life insurance policies

Surrender value is the amount of money that the insurer pays to the policyholder when he surrenders the policy prematurely. Surrender value consists of the returns that the policy has earned plus the surrender value as promised by the policy at inception. According to the new norms introduced by the IRDAI, the surrender value of the policy will calculated keeping in mind the tenure for which the policy was in force. This simply means that the longer the policy tenure more the surrender value.

The surrender value will be calculated as mentioned below:

Non-single premiums

Surrendered in 2nd year = 30% of total premiums paid

Surrendered in 3rd year = 35% of total premiums paid

Surrendered in 4th to 7th year = 50% of the total premiums paid

Surrendered before 2 years of maturity = 90% of the total premiums paid

Single premiums (Single pay policies)

Surrendered in the 3rd year = 75% of total premiums paid

Surrendered in the 4th year = 90% of total premiums paid

Surrendered before 2 years of maturity = 90% of the total premiums paid

The new rules state that the customers, starting from 1st April 2024 will get a lesser amount as surrender value if they surrender their life insurance policy in the first 3 years since the purchase.

Life Insurance Policy: FAQs

1. What is term life insurance?

Term Life Insurance is a simple plan, which takes care of the expenses of your family in your absence in the form of a huge life cover for a very small premium. In case of a policyholder's untimely death, their family or nominee receives the Cover Amount as per the policy. The plan can be customized to one's needs by including add-on benefits.

2. How much life cover do I need to protect my family?

Your cover amount of Term Insurance should be a factor of your family's expenses keeping in mind the inflation as well.

A simple way to calculate is going up to 20x of your annual earnings so as to sufficiently cover your family's financial needs in your absence

3. Do you get your money back at the end of a life insurance policy?

Life Insurance policies offer an option of Return of Premium. In case you choose this option, all the premium paid, excluding GST, is paid back as Survival Benefit, in case the policyholder survives the Policy Term

4. How to file a life insurance claim?

In case of the insured's death, the nominee of the deceased will be able to claim in the following way:

Intimate the insurer about the death as soon as possible with all the important details such as time, place, and cause of death.

Submit needful documents and proof to the insurance company. This will consist of the insured's death certificate along with the claim form provided by the insurance company.

If the policy was assigned, the assignee will have to provide the documents. If someone else (apart from the nominee or assignee) is filing a claim, (s)he has to submit the legal proof of his/her relation with the insured.

If required, post-mortem, hospital, and attending doctor's reports have to be submitted.

In cases involving police inquiries, an investigation/survey report will have to be submitted.

Once the investigation is over, the insurance company will approve/disapprove the claim. The details of the same will be shared with the claimant.

5. Can premiums be tax deductible?

Yes, the premium paid towards the policy is tax exempted up to a maximum limit of Rs 1.5 lakh in a financial year U/S 80C of the Income Tax Act.

6. Can Insurance be cashed in before death?

Yes. Depending upon the cash value of a particular policy, it can be cashed in. Cash value is a part of a life insurance policy's death benefit which can be liquidated. In case the policyholder takes a loan against the cash value and passes away while the loan is unpaid, the death benefit is reduced by the amount of the outstanding loan.

7. Do I need both- Life Insurance and critical illness cover?

It completely depends on your insurance needs. However, it is beneficial to have enhanced insurance coverage and opt for life insurance and critical illness cover both.

8. Does life insurance cover accidental death?

Yes, life insurance policies do cover accidental death. However, one must check the policy documents if it specifically states that it does not cover death by accident.

9. Do Life Insurance Policies offer Grace Period?

Yes. The life insurance policies offer a grace period of 30 days (to pay the premium) in case the policyholder missed his/her premium payment date.

10. How Much Life Cover Can I buy?

The amount of cover depends on your income, your family's requirements, and your liabilities. However, as per the financial experts, your cover should be at least 10-15 times the annual income.

11. How to revive a lapsed life insurance policy?

The IRDA has directed all the insurance providers to allow policyholders to revive their lapsed policy within two years from the time it is deactivated. One needs to pay the renewal fee along with the late fee and additional penalties that may vary from insurer to insurer.

12. What will happen to the life insurance benefit if both the policyholder and nominee dies?

In such scenarios, where both the policyholder and nominee died, then the benefit will be payable to their heirs or legal representative.

13. What to do if my nominee dies before me?

In such a case, you can add a new nominee. In case you don't, by default, the company will consider your heir your new nominee.

14. What is the most cost-effective life insurance type?

A term plan is the cheapest type of life insurance since it does not include any survivor benefits. When the policy period ends, the plan lapses.

15. I have a Life insurance cover of 25 Lakhs. Is it enough?

The thumb rule for choosing the right coverage is getting the cover of 10-15 times your annual income. Therefore, analyze your requirements first, and then decide your ideal life insurance coverage.

16. Should I choose a term life insurance or a whole life insurance policy?

If you are looking for a coverage that lasts for a shorter period of time and buys in affordable premiums then you can buy a term insurance policy. Whereas, if you want coverage for a very long time or for your entire life then go for a whole life insurance policy.

17. What is Return of Premium (RoP) life insurance?

Return of Premium is a feature that you can get with your term life insurance wherein, if you outlive your term insurance policy the insurer pays you back the premiums that you paid in full or partially.

18. What will happen to my life insurance policy if I do not pay my premiums?

If you stop paying for your life insurance policy, your policy will lapse after the grace period and you will lose all the premiums that you have paid.

19. What are the factors that affect my life insurance premiums?

Your life insurance premiums are based on multiple factors such as your age when you decide to buy the policy, lifestyle habits which include smoking and drinking, medical history for existing diseases, gender and the tenure of your policy.

20. Do I have to pay taxes on the receival of my life insurance sum assured?

Since life insurance doesn’t fall into gross income you do not need to report about the amount you receive.

21. What type of life insurance is considered to be best in general?

Although all kinds of life insurance serve different purposes, Term Insurance is said to be the best form of life insurance.

22. Is short term life insurance worth it?

Short term life insurance is known as term insurance. Yes, it is an excellent option as it gives you affordable premium payment options and you get the flexibility of switch or extend your coverage.

I am very grateful to the insurance experts of PolicyX and Mr. Ankur, who kindly helped me settle the claim of Aegon Life Insurance. Thanks again, I& 039;ll always remember this favor.

Prerna Negi

Chennai

April 8, 2024

I bought a Bajaj Allianz Life Insurance through PolicyX, and I must say the level of communication and assistance I have received has been truly impressive.

Preety Kamat

Bhopal

April 8, 2024

Got ICICI Pru iProtect Smart term insurance plan via PolicyX; so far, I& 039;ve hassle-free renewal service and have not faced any kind of nuisance.

Sahani Kaur

Gandhinagar

April 8, 2024

The PNB MetLife Mera Term Plan Plus I& 039;ve bought it at a low premium, and it is fully satisfactory to me. The insurance expert of PolicyX is too polite, and their online buying facility red...

Sneha Nath

Mumbai

March 28, 2024

I would like to inform you that my maturity claims have been settled by SBI Life Insurance on 04.15.2024 and thanks all of you for helping me throughout the claim process.

Khushi Kaur

Chennai

March 28, 2024

I& 039;m writing this review to let you all know that I& 039;m very satisfied because I got my kotak mahindra life insurance policy today as a result of your team effort.

kartik saxena

Goa

March 18, 2024

I had to add some riders to my Sbi life insurance, policy.com team helps to me to understand which rider is more important and which is not. Resulting helps me to save lots of money. Happy with...

Anoop srivastva

Gandhinagar

March 18, 2024

No hidden fees or charges! I have some doubts regarding my PNB MetLife insurance premiums. So I decided to visit policyx.com. Within in couple of minutes, they resolved all of my queries. I am ...

Naval Goel is the CEO & founder of PolicyX.com. Naval has an expertise in the insurance sector and has professional experience of more than a decade in the Industry and has worked in companies like AIG, New York doing valuation of insurance subsidiaries. He is also an Associate Member of the Indian Institute of Insurance, Pune. He has been authorized by IRDAI to act as a Principal Officer of PolicyX.com Insurance Web Aggregator.

Talk to our Trusted Insurance Advisors for Best Plans