While purchasing anything, we always consider having options. Be it everyday gro ...Read More

11+ Years

IRDAI Approved

5M+

Quotes Generated

100K+

Happy Customers

PolicyX is one of India's leading digital insurance platform

11+ Years

IRDAI Approved

5M+

Quotes Generated

100K+

Happy Customers

PolicyX is one of India's leading digital insurance platform

PolicyX Exclusive Benefits

No Spam

No Gimmicks

Personalised

Insurance Advice

24×7

Claim Assistance

Himanshu is a content marketer with 2 years of experience in the life insurance sector. His motto is to make life insurance topics simple and easy to understand yet one level deeper for our readers.

Sharan Gurve has spent over 9 years in the insurance and finance industries to gather end-to-end knowledge in health and term insurance. His in-house skill development programs and interactive workshops have worked wonders in our B2C domain.

Updated on Jun 03, 2026 3 min read

While purchasing anything, we always consider having options. Be it everyday groceries or buying expensive clothes. Wouldn't you agree that comparing plans while buying life insurance is essential too? However, people are always confused between participating and non-participating life insurance policies. You might come across these two terms, making you wonder what is the difference between both?

Let's understand how different these two are and how they can impact your life insurance journey.

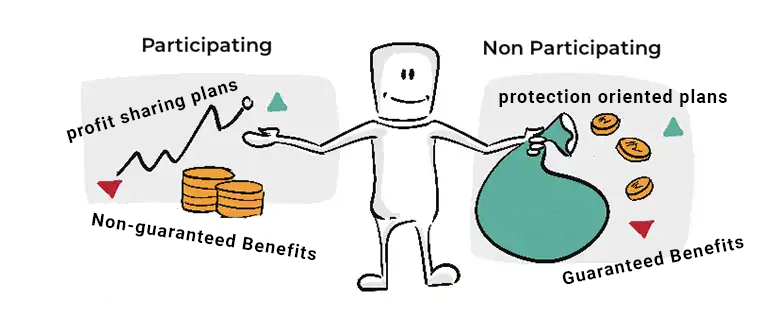

A participating life insurance plan comes with profit-sharing benefits, often referred to as a par policy. When you buy a participating life insurance plan, over the financial year, the company earns specific profits. The insurer pays you some part of the profit as a bonus or dividends via payouts annually, and you can use them to achieve your future financial goals such as:.

A non-participating life insurance plan is solely protection-oriented, and neither does it provide any bonus or dividends from the insurer's profit. It is often referred to as a non-par plan. Under this plan, you do not get any dividend or additional annual payouts.

Please note that most non-participating plans provide a guaranteed maturity benefit. If you know you'll survive the policy tenure, opting for a non-participating life insurance plan would be best for you.

| Participating Plans | Non-Participating Plans |

|---|---|

| The participating life insurance plan comes with profit-sharing benefits. The insurer shares the company profits with the policyholder as a bonus or dividend annually. | A non-participating policy is a contract between an insurer and policyholders where the insured pays premiums in exchange for a death benefit. Please note that these plans do not offer any dividend payouts and offer additional annual payouts. |

| Life insurance plans like endowment and money-back plans are considered participating plans. | A life insurance policy that offers a guaranteed payout at maturity is a non-participating insurance plan. |

| When the insurer earns certain profits, policyholders may receive dividends. This bonus can be used to pay remaining premiums, add-on optional covers, or be taken as cash. | Insured persons do not have a direct say in the company's operations or profit distribution. |

Now, you may understand what the par and non-par policy is. Let's look at the key points that make both plans differ from each other:

Participating and non-participating life insurance plans are designed to serve the different needs of policyholders. Hopefully, with the details above, you'll understand the difference between both kinds of life insurance plans. For further assistance, you can reach out to our insurance experts at PolicyX and get an instant solution in no time.

A life insurance policy that does not offer any market returns, dividends or additional annual payouts but offers a guaranteed payout at maturity is a non-participating insurance plan.

A par-term insurance policy typically costs even more than a non-par-term insurance policy due to the dividend payments.

Yes, premiums are fixed in a non-participating term insurance plan based on the policy contract.

Bonuses or dividends can be used to pay remaining premiums, add-on optional covers, or be taken as cash.

Policyholders may participate in company decisions through voting or representation at annual meetings in participating life insurance.

See More Life Insurance Articles

See MoreLife Insurance Articles