Health Insurance Portability

Switching to a new health insurance plan can be confusing. Many people are concerned that switching insurers will result in losing benefits such as coverage for pre-existing conditions, waiting periods already served, or no-claim bonuses. In India, the insurance regulator IRDAI allows a process called health insurance portability. This process enables policyholders to switch their insurance policy to a new insurer while retaining the benefits they have already earned.

This guide explains what portability is, who can port their policy, what benefits transfer, what does not transfer, how the process works, and important tips to ensure a smooth switch.

What Is Health Insurance Portability

Health insurance portability is the process of moving your existing health insurance policy from one insurance company to another at the time of renewal while retaining the benefits you have already earned. Portability is allowed only at renewal. You cannot switch insurers in the middle of a policy term.

Portability ensures that waiting periods already served for pre-existing conditions, time-bound exclusions, and other benefits are not lost when moving to a new insurer. Portability is a right provided to policyholders by IRDAI to encourage better service and coverage choices.

Example: If your current policy has a two-year waiting period for diabetes and you have completed 18 months, the new insurer will only require you to complete the remaining six months.

Who Can Port Their Policy

Group health policies (employer plans) have restricted portability rules and cannot always be ported freely. This includes individual health insurance plans, family floater plans, and senior citizen health plans. The following rules must be followed to be eligible for portability:

- Your policy must be active when you apply for porting.

- There should be no break in coverage. Even a one-day lapse may make you ineligible for portability.

Benefits That Transfer During Porting

Porting allows you to retain the benefits that you have already earned. These benefits are credited only up to your current sum insured. These benefits include:

- Waiting periods already served: Time already waited for pre-existing or other diseases is credited.

- Time-bound exclusions already serve: Conditions such as cataract, hernia, or piles that had waiting periods in your old policy are recognized by the new insurer.

- No-claim bonus: Some insurers may allow your claim-free bonus to transfer depending on their policy rules.

Benefits That Do Not Transfer During Policy Porting

Not all benefits are carried forward. The following benefits do not transfer:

- Waiting periods already completed apply only to the original sum insured. Any increase in coverage during porting attracts fresh waiting periods under the new policy.

- New add-ons or riders chosen while porting are treated as fresh benefits and come with full waiting periods, even if similar benefits existed earlier.

- Sub-limits, co-payment clauses, and room rent restrictions are as per the new policy terms and do not carry forward from the previous insurer.

- Cosmetic, aesthetic, or optional treatments are covered only if allowed under the new policy, regardless of whether they were included earlier.

Step-by-Step Process to Port Your Policy

The process of porting your health insurance can be completed by following these steps:

- Compare new policies. Look at the sum insured, coverage, sub-limits, room rent, co-payment, and add-ons.

- Apply for portability before the renewal date. The ideal window is 45 to 60 days before expiry, with a minimum of 30 days.

- Fill out portability and proposal forms, providing policy details with policy copy, claims history with documents, and medical history.

- Medical underwriting by the new insurer. Depending on your age, health, and coverage, the insurer may ask for medical tests.

- Receive approval, a counter-offer, or rejection. If your application is rejected, your old policy remains valid.

- Pay the premium and activate the new policy once approval is received.

Understanding Waiting Periods and Premiums

Waiting periods are the most important part of portability. The waiting period you have already served remains valid. Only new benefits or an increased sum insured may attract a fresh waiting period.

Porting may affect your premium. Premiums are determined by age, health condition, sum insured, coverage, add-ons, city, and the pricing structure of the new insurer. Porting is primarily about getting better coverage and service, not necessarily a lower premium. A slightly higher premium may give more comprehensive protection.

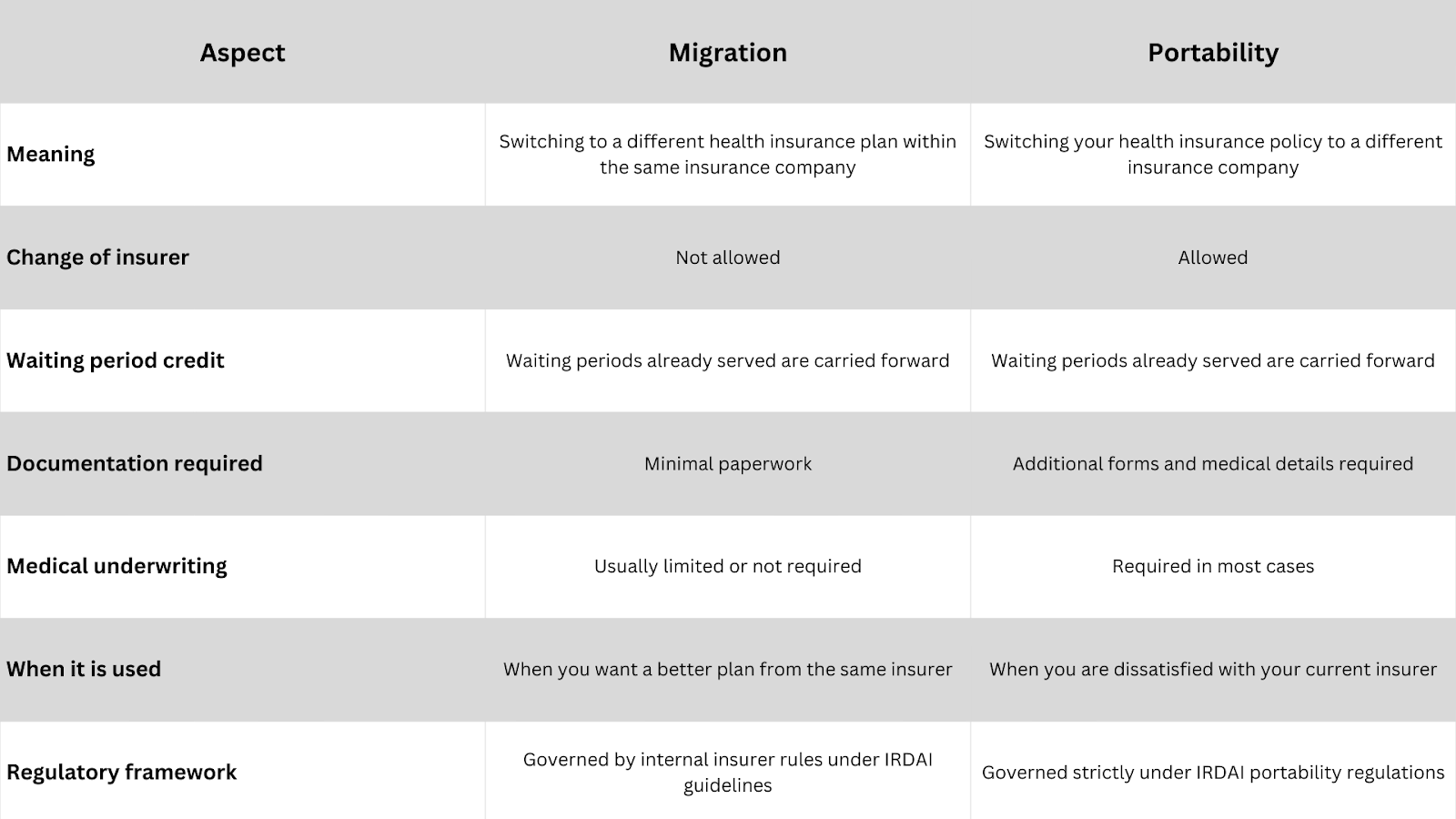

Migration Versus Portability

Migration and portability are different processes. It is important to understand these differences.

Migration allows you to switch to a different policy plan within the same insurer. Portability allows you to switch to a new insurer. Both processes allow waiting period credit, but portability requires additional forms, documentation, and underwriting.

Common Mistakes to Avoid

These are some common mistakes that should be avoided when porting a policy:

- Missing the porting window can lead to rejection of the portability request and loss of waiting period benefits already earned under the existing policy.

- Hiding or misrepresenting medical history may result in claim rejection later, even if the new policy is issued after porting.

- Cancelling the old policy before the new one is approved can create a coverage gap if the portability request is declined.

- Choosing a policy based only on a lower premium may lead to restrictive coverage, higher out-of-pocket expenses, and reduced claim payouts.

- Assuming all benefits transfer automatically is incorrect, as only waiting periods carry forward, while policy features follow the new insurer’s terms.

When Should You Port Your Policy

Porting is recommended if:

- Your current insurer frequently rejects claims

- Coverage is insufficient or outdated

- Room rent limits or co-payments are restrictive

- Customer service is poor

Porting should be avoided if:

- You are currently undergoing active treatment

- Your health risk has recently increased

- The new policy offers only minor or cosmetic improvements

Conclusion

Porting is a policyholder’s right, not a favour. Plan ahead and apply before the renewal date. Keep all relevant documents and claims history readily available. Choose coverage based on your needs, not just premiums. Benefits already earned are safe, but new benefits or an increased sum insured may have fresh waiting periods. By following the process carefully, you can move to a better insurer without losing any of the benefits you have already earned.

If you need assistance porting your policy, you should talk to our advisors at PolicyX.com. We offer no spam, no gimmicks, only expert insurance advice.

Consult for Personalized Insurance Advice

But how does it work?

Schedule a call with India’s number 1 trusted advisor with a 4.5+ rating on Google. We are not your average insurance agents. Our advisors are experts in their insurance knowledge and will give you the right information at the right time. The service is free of cost! Don’t worry, we won’t spam as we value your time.

Health Insurer Network Hospitals

Health Insurance Portability: FAQ

1. How do I transfer my health insurance from one company to another?

You can transfer your health insurance by applying for portability at the time of renewal, at least 45 to 60 days before policy expiry, and completing the new insurer’s proposal and portability forms.

2. What are the disadvantages of porting a mediclaim policy?

Porting may involve medical underwriting, possible premium increase, fresh waiting periods on higher sum insured, and rejection risk if health conditions are considered high-risk.

3. What is the IRDA rule for porting?

IRDAI allows policyholders to switch insurers at renewal while carrying forward waiting periods already served, provided there is no break in policy continuity.

4. What is the waiting period for health insurance portability?

There is no new waiting period for benefits already served, but fresh waiting periods apply to new add-ons or increased sum insured after porting.

5. What is the 3-year rule in insurance?

The 3-year rule means that after three continuous policy years, most non-disclosure related claim rejections become difficult, except in proven fraud cases.

6. What are portability rules?

Portability rules require applying before renewal, maintaining continuous coverage, full medical disclosure, and acceptance by the new insurer after underwriting.

7. How many times can health insurance be ported?

There is no limit on the number of times you can port a health insurance policy, as long as you follow IRDAI rules and maintain continuity.

8. When should I apply for portability?

You should apply at least 30 days before renewal, ideally 45 to 60 days earlier, to allow enough time for underwriting and approval.

9. What is the 80/20 rule for health insurance?

Some policies may have co-payments (e.g., 10–20%), but it is policy-specific, not a universal rule.

10. What are the benefits of porting health insurance?

Porting allows you to change insurers while retaining waiting period benefits, improving coverage, removing restrictive limits, and accessing better service.

11. Who are the top 5 health insurance companies in India?

There is no single official ranking, but leading insurers are usually identified based on claim settlement ratio, service quality, product range, and customer experience.

12. What are the benefits of portability?

Portability protects your accumulated policy benefits, ensures continuity of coverage, and gives you the freedom to move to a better insurer without starting over.

Health Insurance Companies

Know More About Health Insurance Companies

Health Insurance Articles

Standalone Health Insurance Companies Aug, 2024

Inpatient vs Outpatient Aug, 2024

Diseases Covered By Bajaj Allianz Aug, 2024

Diseases Covered By Aditya Birla Aug, 2024

Sum Insured in Insurance Aug, 2024

Yearly Health Insurance Premium Increase Aug, 2024

See More Health Insurance Articles

Bima Insurance Trinity Feb, 2025

Health Insurance Waiting Period Aug, 2024

Health Insurance for Gen Z May, 2025

AI In Health Insurance Apr, 2025

Health Insurance Budget Aug, 2024

See MoreHealth Insurance Articles