Primary Insured in Health Insurance

When you purchase a health insurance plan, one of the key concepts you will encounter is the Primary Insured. This may sound like a simple term; however, this decides who owns the policy, who controls it, and how benefits and claims are processed.

Selecting the best individual as the primary insured can save subscribers money, streamline claims processing, and grant uninterrupted access to medical treatment and healthcare services for the family.

Who Is the Primary Insured in a Health Insurance Plan?

In every health insurance policy, the primary insured is the individual listed on the policy. The primary insured owns the policy, pays the premium, and represents all family members covered under the policy.

If you purchase an individual health insurance policy, you are automatically the primary insured whereas in a family floater health insurance plan, there will be one person listed as the primary insured, and the other family members will be listed as dependents of the primary insured.

For example Amit, 38, buys the Niva Bupa Aspire Gold+ Plan with a sum insured of ₹10 lakh for himself, his wife, and their daughter. The annual premium for this plan is ₹8,482 in Delhi (about ₹707 per month). Since the policy is in Amit’s name, he is the primary insured.

If his daughter is hospitalized for ₹2.5 lakh, the hospital verifies Amit’s details as the primary insured before processing the claim. The claim is settled directly with the hospital through Niva Bupa’s cashless hospital network.

Responsibilities of the Primary Insured

The primary insured is responsible for ensuring the policy stays active and effective. However, family members may also be involved with certain tasks, like updating contact information or adding dependents.

Policy Management

The primary insured must pay premiums on time and renew the policy before the due date to prevent lapses in coverage.Communication with the Insurer

All policy documents, renewal alerts, and claim notifications are sent to the primary insured’s registered email or phone number.Adding or Removing Family Members

Only the primary insured can add new members, such as a newborn, or remove dependents when required.Filing and Tracking Claims

During hospitalization, the primary insured is the point of contact for hospitals and the insurance company.Claiming Tax Benefits

The person who pays the premium, usually the primary insured, can claim tax deductions under Section 80D of the Income Tax Act.

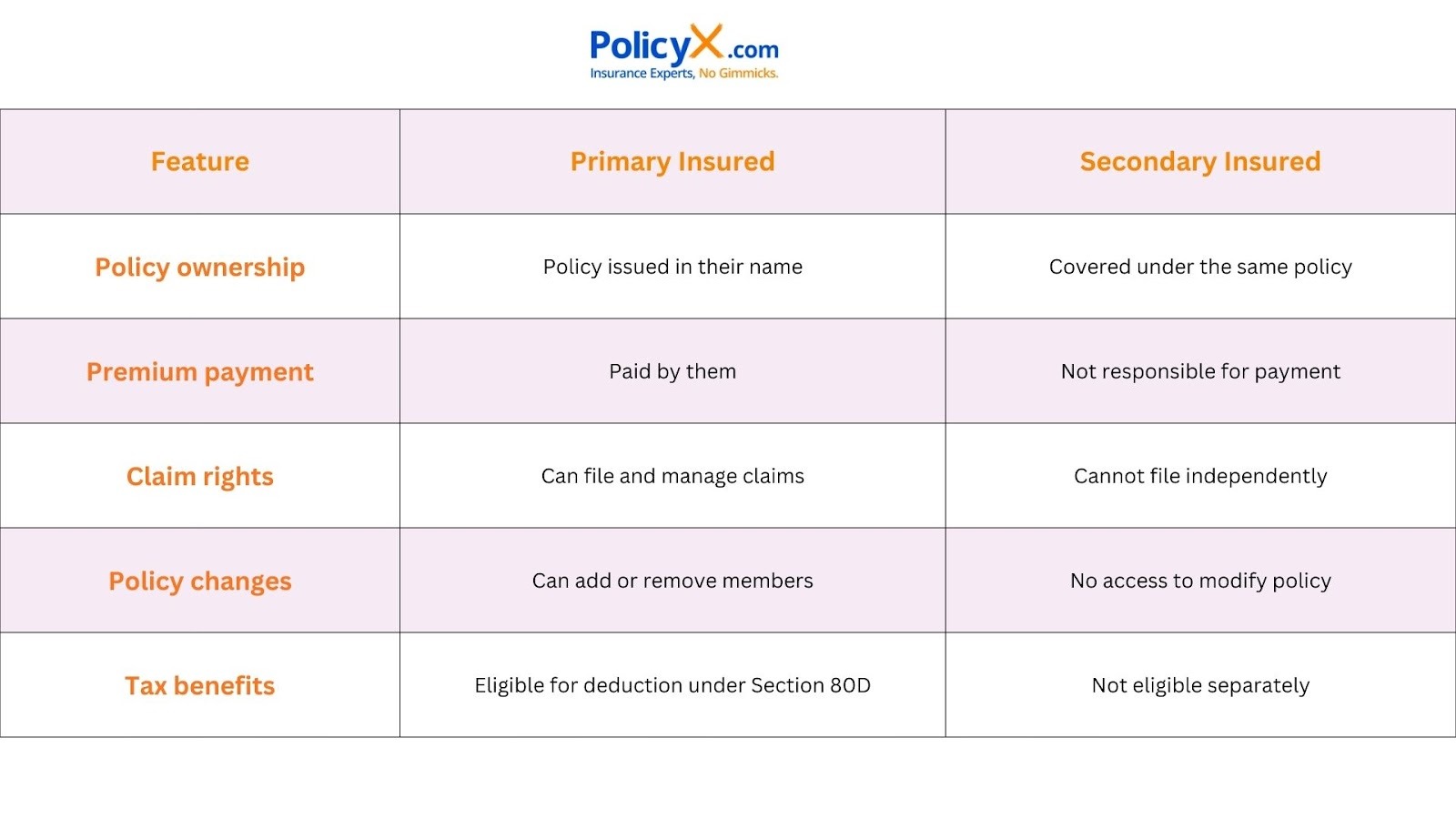

Primary Insured vs Secondary Dependant

It is important to understand the difference between the primary insured and dependents. The table below differentiates the two based on several features.

Benefits of Being the Primary Insured

The person who is the primary insured in a health insurance policy receives several benefits.

- The primary insured is entirely responsible for the policy and determines the sum insured, add-ons, and features.

- Claims are validated using the primary insured’s details, allowing for quicker processing.

- The primary insured can claim tax deductions amounting to ₹25,000 under Section 80D or up to ₹50,000 if the plan covers senior citizens.

- All records, renewals, and claims are tied to the primary insured, which simplifies the management of the policy.

- Designating a younger person as the primary insured will reduce the premium while still maintaining equal coverage.

How to Choose the Right Primary Insured

- In family floater policies, the premium is based on the age of the oldest member. Choosing the younger adult as the primary insured helps reduce costs. For Example: Ritu, 35, and her husband, 40, buy the Star Health Family Health Optima Plan with a ₹10 lakh sum insured. If Ritu is the primary insured, the annual premium is ₹27,500. If her husband is listed instead, it increases to ₹31,000.

- Selecting the younger member as the primary insured helps maintain lower premiums.

- The person who pays the premium and files taxes should ideally be the primary insured to claim benefits.

- If one spouse has employer-provided coverage, make the other spouse the primary insured under your personal policy for better risk diversification.

- Choose someone who can easily respond to insurer calls or hospital verification requests during emergencies.

Common Mistakes to Avoid

Given below are some common mistakes that you need to avoid while you are listing the primary insured in a health insurance policy.

- Listing the oldest family member as the primary insured. This increases premiums.

- Not transferring ownership after the primary insured’s death.

- Forgetting to update contact details causing claim or renewal delays.

- Assuming anybody other than the prime insured can file claims.

- Missing renewal payments leads to policy lapses.

Important Clarifications About the Primary Insured

- The primary insured manages the policy but does not receive exclusive coverage; all insured members get equal benefits.

- Claims are not approved or rejected based on who is the primary insured.

- Dependents can receive treatment and claims are processed without the primary insured being hospitalized.

- The primary insured’s physical presence is not mandatory during emergencies.

- Changing the primary insured, when approved by the insurer, does not reset waiting periods or cancel continuity benefits.

- The primary insured does not have to be the eldest or highest earner; younger members often help keep premiums lower.

- While the primary insured and policyholder are usually the same person, the policyholder can sometimes be someone who manages the policy for others, like a parent or guardian for their children.

How the Primary Insured Affects Claim Settlement

The primary insured’s details are essential for every claim, whether it’s cashless or reimbursement.

Cashless Claim Example: Under the Niva Bupa Aspire Gold+ Plan, if Amit’s wife undergoes a ₹2.8 lakh surgery at a network hospital, the hospital first verifies Amit’s details as the primary insured. Once approved, Niva Bupa settles the bill directly with the hospital.

Reimbursement Claim Example: If the treatment is at a non-network hospital, Amit files a claim using his documents as the primary insured. Once approved, the settlement amount is credited to his bank account.

Conclusion

The primary insured is the basis for every health insurance. They manage the policy, handle renewals, and are the first point of contact for medical claims. Choosing the right person as the primary insured can help you lower premiums, simplify the claims, and make sure your family can always have access to great medical facilities.

Before you finalize your policy, make sure to review whose name is the primary insured. This simple act can have a huge impact on you or your loved ones when you need financial protection for medical treatments.

To know more about the best health insurance policies, visit PolicyX.com. We offer no spam, no gimmicks, only expert insurance advice.

Consult for Personalized Insurance Advice

But how does it work?

Schedule a call with India’s number 1 trusted advisor with a 4.5+ rating on Google. We are not your average insurance agents. Our advisors are experts in their insurance knowledge and will give you the right information at the right time. The service is free of cost! Don’t worry, we won’t spam as we value your time.

Health Insurer Network Hospitals

What Is Primary Insured in Health Insurance? A Complete Guide for Policyholders: FAQ

1. What is a primary insured in a health insurance policy?

The primary insured is the person in whose name the policy is issued and who owns, manages, and controls all aspects of the health insurance plan.

2. Why does choosing the right primary insured matter?

Because premiums, policy control, claim verification, and insurer communication are all linked to the primary insured’s details.

3. Who can file and manage health insurance claims?

Only the primary insured can officially file, track, and manage claims, even when treatment is for a dependent.

4. How does the primary insured affect the premium amount?

In family floater plans, premiums are based on age, so selecting a younger primary insured usually results in lower premiums.

5. What happens if the primary insured is not the one hospitalized?

The claim remains valid, but hospitals and insurers verify the primary insured’s information before approving or settling the claim.

6. When can the primary insured be changed in a policy?

The primary insured can be changed in cases like death, divorce, or on request, subject to insurer approval and required documentation.

7. Who can claim tax benefits on a health insurance policy?

The person who pays the premium can claim tax deductions under Section 80D, which is usually the primary insured.

Health Insurance Companies

Know More About Health Insurance Companies

Health Insurance Articles

Janani Suraksha Yojana Aug, 2024

No Waiting Period In Maternity Aug, 2024

Employee State Insurance Aug, 2024

Central Govt. Health Scheme Aug, 2024

Care Policy & Claim Status Aug, 2024

Niva Bupa Claim Status Aug, 2024

See More Health Insurance Articles

Bima Insurance Trinity Feb, 2025

Health Insurance Waiting Period Aug, 2024

Health Insurance for Gen Z May, 2025

AI In Health Insurance Apr, 2025

Health Insurance Budget Aug, 2024

See MoreHealth Insurance Articles